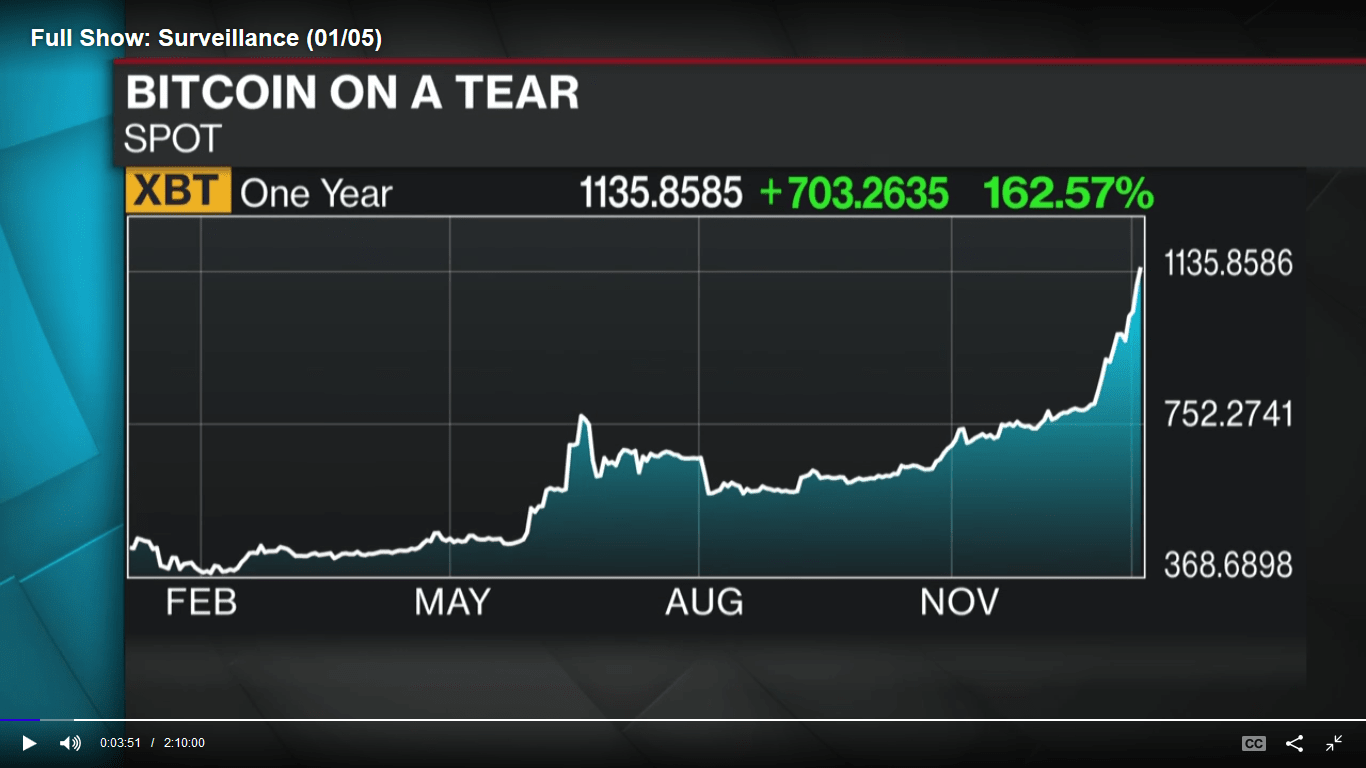

I’d heard of Bitcoin, mostly in relation to the dark web, and I thought it was a yesterday thing. I woke  up smartly on Wednesday when I saw that its value has risen by 163% and doubled in the last two months of 2016. It’s driven by the Chinese—but also countries like India and Venezuela who are worried about their currencies. It may even be replacing gold as a store of value.

up smartly on Wednesday when I saw that its value has risen by 163% and doubled in the last two months of 2016. It’s driven by the Chinese—but also countries like India and Venezuela who are worried about their currencies. It may even be replacing gold as a store of value.

I hadn’t, however, heard about much about its underlying technology, Blockchain, until my pal in Australia, Geoff G, suggested I look at it. Blockchain is likely to change our lives in many areas, way beyond accounting!

If, like me, it’s new to you, here’s an idiot’s guide to it.

After I’d watched that I understood a bit—but not enough to make the link between it, budgets and forecasting. The financial link is because the Blockchain is the revolutionary concept that drives Bitcoin—and an increasing number of applications.

Satoshi Nakomoto created Bitcoin in 2008: a peer-to-peer electronic cash system that allows online payments to be transferred directly: no intermediary required. It is to Blockchain what email is to the Internet and there are currently about 700 other applications.

Collin Thompson in Intrepid Review describes it thus: “Blockchain is a type of distributed ledger or decentralized database that keeps records of digital transactions. Rather than having a central administrator like a traditional database, (think banks, governments & accountants), a distributed ledger has a network of replicated databases, synchronized via the internet and visible to anyone within the network. Blockchain networks can be private with restricted membership similar to an intranet, or public, like the Internet, accessible to any person in the world.”

Until Blockchain introduced transparency, it was impossible to do direct financial transactions over the net, because essentially you are transferring files, which are easy to copy and thus you could either steal the data or double spend the money, hence the need for a trusted intermediary, like a bank.

“When Blockchain carries out a digital transaction, it is grouped together in a cryptographically protected block with other transactions that have occurred in the last 10 minutes and sent out to the entire network. Miners (members in the network with high levels of computing power) then compete to validate the transactions by solving complex coded problems. The first miner to solve the problems and validate the block receives a reward. (In the Bitcoin Blockchain network, for example, a miner would receive Bitcoins).

“The validated block of transactions is then time-stamped and added to a chain in a linear, chronological order. New blocks of validated transactions are linked to older blocks, making a chain of blocks that show every transaction made in the history of that Blockchain. The entire chain is continually updated so that every ledger in the network is the same, giving each member the ability to prove who owns what at any given time.”

“Blockchain has applications that go way beyond obvious things like digital currencies and money transfers. From electronic voting, smart contracts and digitally recorded property assets to patient health records’ management and proof of ownership for digital content.

“Blockchain will profoundly disrupt hundreds of industries that rely on intermediaries, including banking, finance, academia, real estate, insurance, legal, health care and the public sector — among many others. This will result in job losses and the complete transformation of entire industries. But overall, the elimination of intermediaries brings mostly positive benefits.

“Banks and governments for example, often impede the free flow of business because of the time it takes to process transactions and regulatory requirements. The Blockchain will enable an increased amount of people and businesses to trade much more frequently and efficiently, significantly boosting local and international trade. Blockchain technology would also eliminate expensive intermediary fees that have become a burden on individuals and businesses, especially in the remittances space.” Thanks Collin. He is the co-founder of Intrepid Ventures, a Blockchain startup and innovation studio.

David Lyford-Smith of the ICAEW’s IT Faculty says :

“In order to work as a major element of the financial system, the market needs to invest in research. It is not yet known how the complex work of processing new transactions in a blockchain can be scaled up to the volumes and timescales necessary,” and goes on to state that “Despite holding billions of dollars, the current bitcoin chain can only handle five to six transactions per second across the entire network, often with latency of several hours.”

Lyford-Smith cautions “One key issue with blockchain is its reputation. Separating the technology from the bitcoin roil is an important first step!”

If you don’t have to pay bank charges, employ consultants and lawyers to ensure you are not being ripped off, what’s that going to do to your bottom line? Forecast5 is ready to help you. Download our free 21-day trial here.

**************************************************

Some interesting background reading and watching – and the first is like a “who dunnit”:

How Blockchain technology has been used to fight fraud; Ted Talks – Kathryn Haun, US Prosecutor

Blockchain is eating Wall Street; Ted Talks – Alex Tapscott, Author of the “Bitcoin Revolution”,

New Kids on the Blockchain, Ted Talks – Lorne Lantz

At the Speed of Money; How Cryptocurrency Will Transform Everything, Ted Talks – David Morris

How Blockchain will impact Accountants and Auditors – ICAEW Economia

Bank of England – Accelerator Project – Distributed Ledger Technology